Featured

Growth, Profitability, and the “Rule of 40” for Private SaaS Companies

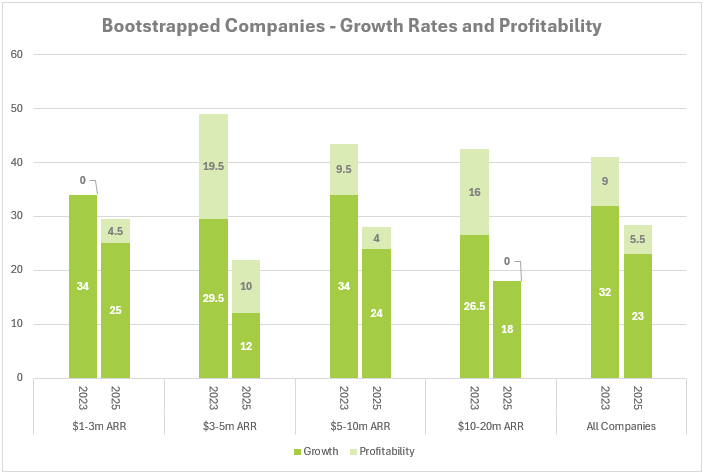

The Rule of 40 is not a perfect metric, but it remains a useful lens on SaaS company performance. Growth continues to be the dominant driver, though profitability trends are shifting as equity-backed companies reduce burn. Bootstrapped companies still hold the edge on this metric, but the gap is narrowing.